(Note: the below is a high level review of certain potential issues and is not to be relied upon in any definitive manner nor as legal and/or regulatory advice).

Consumer law and e-money / payment businesses

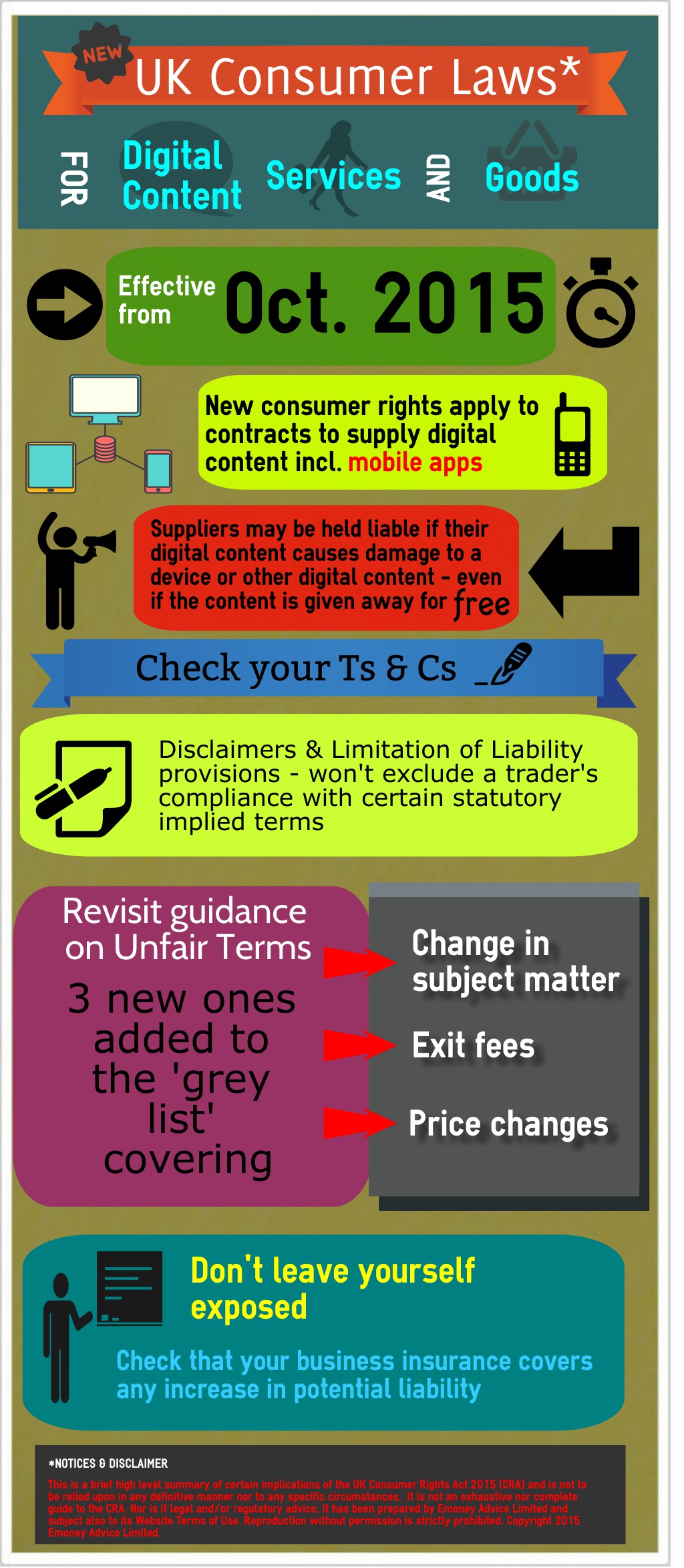

Consumer law continues to evolve, most notably in the UK with the enactment of the Consumer Rights Act 2015 (CRA) – to be largely brought into force in October 2015.

Together with specific payment and financial services regulations, compliance with most general consumer law is also required of consumer payment businesses.

Regulators are more than ever paying specific scrutiny on a firm’s ability to satisfy their obligations to these customers – as such supervisors look to meet their own consumer protection objectives.

Specific UK consumer laws

In general terms, some of the key UK laws that a consumer e-money / payment services business needs to carefully consider include:

- The consumer protection provisions under the Payment Services Regulations 2009 and the Electronic Money Regulations 2011 (as applicable)

- The Financial Services (Distance Marketing) Regulations 2004 (or if otherwise applicable – the Consumer Contracts (Information, Cancellation and Additional Charges) Regulations 2013)

- Consumer Protection from Unfair Trading Regulations 2008

- The Provision of Services Regulations 2009

- The following “pre-CRA” laws, which as indicated below will change with the CRA

|

Pre- CRA |

Post CRA |

| Unfair Contract Terms Act 1977 (UCTA) | Amended. The CRA will contain merged the consumer contract rules set out in UCTA and UTCCR. |

| Unfair Terms in Consumer Contracts Regulations 1999 (UTCCR) | Revoked – see above. |

| Supply of Goods and Services Act 1982 | Amended. The CRA will contain the consumer rules on service standards, performance, consumer contract remedies (+ hire contracts). |

| Sale of Goods Act 1979 | Amended. The CRA will contain the rules on implied terms, rights to reject remedies, together with terms on delivery and passage of risk. |

| Sale and Supply of Goods to Consumer Regulations 2002 | Revoked. The CRA will contain consumer guarantee provisions. |

What is the impact of the CRA to e-money and payment services businesses?

The short answer is that it is pretty much the same as to other consumer facing businesses. The CRA will both supplement and consolidate existing UK consumer law, with some of its key features including:

- New rules expressly applicable to “Digital Content“ – this will include mobile apps. Please note that the new laws may increase legal exposure. For example, even if a trader provides digital content (such as an app) to consumers under contract for free – they can still be held liable under certain circumstances if the digital content causes damage to any device or other digital content

- Wider implied terms – the CRA gives contractual status to certain information provided by a trader

- Implied terms will not fall within exclusion clauses – the CRA expressly prohibits a trader from excluding liability for certain implied terms, and

- Consolidating consumer ‘unfair terms’ – with 3 new ‘grey list’ terms being added. See the CMA’s guidance for more information.

How should e-money / payment services businesses prepare for the CRA?

Some of the key areas to be considered in anticipation of the CRA include:

- Review your product and service offering – note which parts of your offering involves the provision of digital content, services and goods (if applicable) to determine which new rules apply in each circumstance.

- Review your consumer terms and conditions – with particular care to review:

- any disclaimers, exclusions and/or other limitation of liability provisions

- the use of plain language

- the placement of key terms such as price and the subject matter

- whether you can split out obligations under your terms between customers that do and don’t fall under the new statutory definition of consumer, and

- compliance with the revised list and guidance on unfair terms.

- Review any website / promotional / general information provided to consumers – as noted above, these could form part of the consumer contract as implied terms.

- Review insurance arrangements – to ensure that any increases in liability are covered by general business insurance.